Search for any article about raising money for a startup, and they all share a common theme: don’t raise money from “non-accredited investors.” This won’t be one of those articles. The theme here is different: raising money from non-accredited investors is risky, potentially costly, and potentially time consuming. But it’s not impossible.

This article provides an overview of certain laws governing the offer and sale of “securities” (essentially, ownership interests in a company) and the types of startup financings you’ve likely heard about elsewhere. It explains the added risks of fundraising from non-accredited investors. And, finally, it provides some context and insight regarding the original purpose of U.S. federal securities laws that helps explain why raising money in the U.S. can be a burdensome initiative.

This article does not address crowdfunding, another avenue through which non-accredited investors might participate in startup fundraises.

How securities laws operate in the United States.

As a general rule, Section 5 of the United States Securities Act of 1933 (the “Securities Act”) requires that any offer or sale of securities must be registered with the Securities and Exchange Commission (the “SEC”). The SEC registration process is complex, time-consuming, and costly, involving lengthy financial and risk disclosures and filings, such that no early-stage company could reasonably afford to comply with the registration requirements.

Section 4(a)(2) of the Securities Act provides the most-commonly utilized exemption from Section 5. It exempts from SEC registration any “transactions by an issuer not involving any public offering.” At first, this might seem like any private offering is permissible. However, the Securities Act itself provides little clarity regarding the scope of public offerings and what constitutes a permissible “private” offering. As such, any company that tries to comply with 4(a)(2) exposes itself to risks that the SEC will categorize an offering as public and therefore subject to the registration requirements of Section 5. Failure to comply with these requirements can result in both civil and criminal penalties. Understandably, there have been numerous legal disputes about the categorization of securities offerings under 4(a)(2).

To resolve these disputes, courts have created a set of factors that influence whether or not an offering is deemed private. The factors are flexible, and no single factor is determinative.

- The number of investors and their relationship to each other and to the company. The more investors you offer securities to, the less likely the offering is private. Similarly, if you sell securities to investors you never knew prior to discussing or negotiating an investment, that looks like a public offering.

- The number of securities offered and the amount of money you raise. The more securities you offer and the more you raise, the more the offering looks public.

- How the offering is communicated and advertised. Broadly distributing information about the offering likely makes it public. Pitching your company’s offering at a conference also looks public. Having targeted conversations with knowledgeable investors and strategic partners appears private.

- Whether the investors are financially sophisticated and/or experienced investors. It’s usually sufficient that the investors have (a) general business knowledge and experience, (b) the financial ability to bear the risks of their investment, or (c) a special relationship with the company (i.e. a director or officer of the company).

- Information provided or made available to investors. If the company provides (or the investors have ready access to) information outlining the financials and risks of the company, the court might lean in your favor. Although this has nothing to do with the public or private nature of the financing, it aligns with the purpose of SEC regulations (discussed below).

- Actions taken to prevent resale of the securities. If investors can turn around and resell their securities to the public, your original offering looks public. In general, the securities must not be available for resale by the investors, and most purchase documents (along with any other documents certifying an investor’s ownership of the securities) usually include specific representations and disclaimers about restrictions on resale.

The complex and nuanced nature of this analysis explains why 4(a)(2) isn’t necessarily an easy way to exempt a financing round from SEC registration requirements. In order to avoid a lawsuit with the SEC, expensive and time-consuming litigation, and the risks of fines and penalties, a company would need to clearly and conspicuously demonstrate that it addresses the above factors each time it offers or sells securities to investors.

It’s also worth remembering that the U.S. has multiple systems of law. Federal law (such as the Securities Act) governs activity throughout the country. Additionally, each state has its own rules and regulations about activities within its borders. Companies must comply with both federal law and the securities laws of each state where an investor resides. These state securities laws, known as “blue sky laws,” can differ greatly from one another. Complying with each state’s law adds to the cost, time, and risk associated with any securities offering.

How do companies reasonably comply with 4(a)(2)?

To provide clear avenues for companies to privately sell securities under 4(a)(2), the SEC passed certain regulations that operate as “safe harbors.” If a company conducts an offering in accordance with one of the safe harbors, that offering is deemed compliant with 4(a)(2). Compliant offerings are not subject to the multifactorial, flexible test generally applicable to private offerings, and companies do not need to register complaint offerings with the SEC. Instead, a company files a notice (called a “Form D”) informing the SEC of its compliant offering. These safe harbour offerings are commonly referred to as Regulation D offerings.

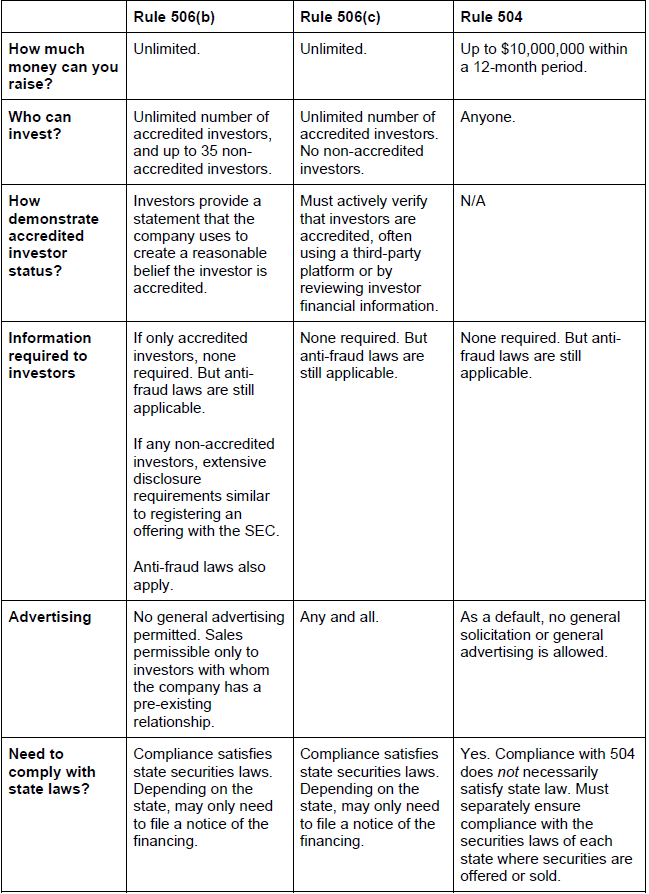

The three most common types of Regulation D offerings are Rule 504, Rule 506(b), and Rule 506(c) offerings, named after the section of Regulation D where the applicable provisions are outlined. Some key differences between these offerings are outlined in the table below.

Notably, either form of a 506 offering is practically limited to accredited investors. (Although a 506(b) offering can include non-accredited investors, but doing so imposes burdensome information disclosure requirements.) 506 offerings fortunately trump state securities requirements: if an offering satisfies 506(b) or 506(c), the company does not need to separately comply with state securities laws except to file any applicable notices of the filing.

Rule 504 permits fundraising from non-accredited investors without imposing substantial information disclosure requirements, however, a 504 offering does not necessarily satisfy state securities laws. As such, a company relying on Rule 504 must separately satisfy the securities laws of each state where securities are offered or sold.

There are several ways an investor can qualify as an “accredited investor”, and satisfaction of the regulatory definition depends, in part, on whether an investor is an individual or an entity. For individual persons, one of the following must apply:

- The investor enjoys a net worth of at least $1,000,000 not including the value of the primary residence.

- The investor had income of at least $200,000 per year for the past two years and expects to make that much during the current year. If an investor has a spouse or a spousal equivalent (defined as a “cohabitant occupying a relationship like a spouse”), their incomes could be combined to reach a $300,000 threshold.

- The investor is a director or executive officer of the company (i.e., has a policy-making function).

- The investor has a specialized license that demonstrates financial savvy.

- The investor is a “knowledgeable employee” of a fund issuing the securities.

There are several types of entities that qualify as accredited investors. However, most applicable here are the following:

- Entities of which all the owners are accredited investors.

- A self-directed ERISA investor benefit plan with investment decisions made solely by accredited investors.

Based on this definition, in most situations, only wealthy individuals or entities qualify as accredited investors. Any investor who does not meet this definition is considered “non-accredited.”

To recap, if a company wants to raise money from a non-accredited investor, it has two primary options. First, the company can offer securities under Rule 504 at the federal level and separately comply with the state securities laws of each state where you offer or sell securities. If you have few investors who reside in one or two states with light regulations, this may be a feasible option. However, with a sizeable number of investors who reside in a patchwork of states, compliance with state laws is costly and time consuming. Your legal team will need to research in detail the laws of each applicable state, manage appropriate communication with investors to comply with differing laws, and facilitate state filings to ensure compliance.

The second option is to forego reliance on any SEC safe harbor and structure your financing pursuant to the general multifactor test courts use to categorize 4(a)(2) private placements. This would involve the same complexities of a 504 financing and expose a company and its officers to risks that the SEC and/or a court deems the financings public (and therefore in violation of SEC registration requirements).

It’s important to remember that securities laws govern both the offer and sale of securities. Companies should discuss with an attorney any applicable securities laws before they begin offering securities to potential investors. Even if a company doesn’t actually sell securities, it could still violate securities laws through a non-compliant offer, advertisement, or publication.

Why are U.S. securities laws so burdensome?

The U.S. federal government created the modern webwork of securities laws in response to the 1929 stock market crash and the subsequent Great Depression. Prior to the stock market crash and the enactment of the Securities Act, companies and securities brokers freely advocated and solicited investors to purchase stock based on grandiose pitches promising rich profits. Investors rarely asked for or received much information about companies or their financial conditions. Promises made by companies and brokers sometimes had little or no substantive basis. In fact, they were often false or misleading. The stock market existed in a state of speculative frenzy and crashed in October 1929 when panicked investors sold off investments en masse.

Congress passed the Securities Act and related laws to guard against economic uncertainty attributed to the misinformation, fraud, and ignorance that permeated the stock market in the 1920s. As such, the primary aim of federal securities law is to ensure investors receive information about the securities they buy and the companies that issue those securities sufficient for those investors to make sound financial decisions. Federal securities laws primarily accomplish this by requiring companies to disclose information about themselves and the securities they issue. The efficacy of these disclosure requirements is backed up by extensive liability for fraud under the Securities Act and the Exchange Act of 1934 for both issuers and sellers of securities. Congress intended to ensure that investors had access to balanced, non-fraudulent information. Any exemption from this default requirement is intentionally narrow. For example, Rules 506(b) and 506(c) of Regulation D specifically address accredited investors because, in theory, accredited investors will know what financial, business and legal information to request from a company they are considering investing in and, therefore, do not need the SEC’s protection from unscrupulous sellers of securities.

It’s certainly debatable whether securities laws have safeguarded investor interests. They have undoubtedly limited investment opportunities in ways that favor wealthy, “sophisticated” investors, cutting off opportunity for those who do not satisfy the SEC’s criteria for sophistication. Nevertheless, raising money from such non-accredited investors is still possible even if it involves increased risks and complexities.

Headquartered in the Research Triangle region of North Carolina, Fourscore Business Law serves entrepreneurs and businesses in the Triangle, throughout the Southeast and in Silicon Valley / San Francisco. We also represent venture capital funds and other investors who invest in companies throughout the U.S. The idea of delivering maximum impact in a simple and succinct manner is what we’re calling the Fourscore Principle. And that is what Fourscore Business Law is based on. Our clients operate in a broad range of industries including tech, IoT, consumer products, B2B services and more. Questions? Shoot us an email or give us a call at (919) 307-5356. Your first call is on us.