By: Benjamin Jacob

On June 5th, the federal government enacted the Paycheck Protection Flexibility Act (the “Flexibility Act”) in response to a wave of criticism across industries and mounting lawsuits over the PPP’s rollout. In the past several weeks, the United States Treasury and Small Business Administration have also issued two Interim Final Rules both implementing the Flexibility Act and offering important new criteria for PPP borrowers.

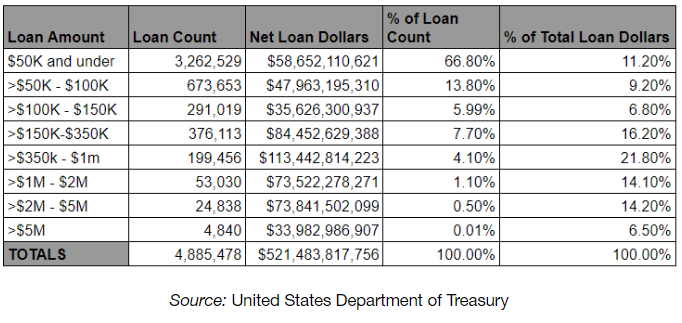

In this post, we’ll take a brief look at some PPP loan numbers recently released by the Treasury and then dive into an overview of the key changes introduced by the Flexibility Act and the guidance provided in the Treasury’s Interim Final Rules.

PPP PROGRAM LOAN BREAKDOWN – BY THE NUMBERS

As of July 7th, 2020, the Paycheck Protection Program (PPP) has backed 4.9 million loans to American businesses totaling approximately $521 billion dollars.

FLEXIBILITY ACT AND INTERIM FINAL RULES – KEY CHANGES AND GUIDANCE

1. Program Extended. The deadline to apply for a PPP loan is now August 8, 2020.

2. Extended Maturity Date. Loans made after June 5th, 2020 will receive an extended maturity date (5 year term versus the original standard 2 year term). For loans originating prior to June 5, 2020, borrowers and lenders will need to review and decide whether the loans will receive the extended 5 year term.

3. Loan Forgiveness Period Increased. For loans issued prior to June 5, 2020, borrowers will have the option to choose either an 8 week or 24 week period for forgiveness eligibility. Loans issued after June 5, 2020 automatically must use the 24 week period.

4. 60/40 Ratio Forgiveness Requirement – Payroll Costs. Originally, PPP borrowers were required to spend at least 75% of their loan proceeds on payrolls costs. The Flexibility Act has decreased this requirement to 60%. From the program’s inception, there has been widespread confusion as to whether this requirement was a threshold for obtaining any loan forgiveness or rather a proportional cap on how much of the loan could be forgiven.

- In its Interim Final Rules, the Treasury has clarified it will be interpreting this requirement as a proportional limit, not a threshold.

- This means that borrowers that spend less than 60% of their PPP loans on non-payroll costs will still be eligible for forgiveness although the forgiveness amount will be reduced proportionately.

- What remains the same is that to be eligible for 100% forgiveness on both the loan principal and interest, PPP borrowers must spend at least 60% of the loan proceeds on payroll costs and the remaining 40% on other eligible uses.

5. EIDL – PPP Loan Refinance Requirements. The Treasury further clarified potential refinance requirements for borrowers who receive an EIDL loan and a PPP loan.

- Borrowers who received their EIDL loan between January 31, 2020 and April 3, 2020 and used the proceeds to cover payroll costs must use their PPP loan to refinance the full amount of their EIDL loan. Importantly, this refinance requirement does not cover EIDL advances (also referred to as an EIDL “grant”) since advances are not required to be repaid. However, any EIDL advance up to $10,000 will be deducted from the PPP loan forgiveness amount.

- Borrowers who received their EIDL loan between January 31, 2020 and April 3, 2020 but used the proceeds only to cover non-payroll costs are not required to refinance their PPP loan.

- Borrowers who received an EIDL loan before January 31, 2020 and after April 3, 2020 are not eligible to refinance their EIDL loan with their PPP loan.

6. Loan Forgiveness Deadline. PPP borrowers must submit their loan forgiveness application within 10 months from the end of the applicable 8 or 24 week forgiveness period. Failure to submit within this time frame will result in borrowers needing to begin repayment of the principal and interest on the loan.

7. New PPP Borrower Application. Available here: SBA PPP Loan Application [New]

Headquartered in the Research Triangle region of North Carolina, Fourscore Business Law serves entrepreneurs and businesses in the Triangle, throughout the Southeast and in Silicon Valley / San Francisco. We also represent venture capital funds and other investors who invest in companies throughout the U.S. The idea of delivering maximum impact in a simple and succinct manner is what we’re calling the Fourscore Principle. And that is what Fourscore Business Law is based on. Our clients operate in a broad range of industries including tech, IoT, consumer products, B2B services and more. Questions? Shoot us an email or give us a call at (919) 307-5356. Your first call is on us.