How a Down Round Affects a Startup Capitalization Table

Some startups occasionally face financial challenges that require the company to sell stock at a lower valuation than the valuation used during a previous stock financing. These fundraising rounds are often referred to as “down rounds.” Besides representing a potential setback in a company’s apparent growth, down rounds can affect a company's “as-converted” equity ownership structure by adjusting how preferred stock might convert into common stock upon a sale of the company or other liquidation event.

Here, we provide a brief overview of the factors affecting company valuations, preferred stock conversion mechanics, and the effect of a down round on equity ownership.

Why do down rounds happen?

As businesses grow, we expect the value of the company to increase and that the company will close subsequent funding rounds at correspondingly higher prices. However, the actual valuation of a company is subject to myriad variables, including its satisfaction of (or failure to meet) benchmarks, unforeseen competition, customer acquisition, and general market trends affecting investors’ willingness to make high-risk investments. If these factors diminish a company’s existing valuation, an investor may only participate in a new stock financing if shares are offered at a lower price than that of any previously-issued shares.

Additionally, while early investors in startup companies usually buy at the lowest prices, subsequent investors can better assess whether or not companies have met stated benchmarks such as product development, key hires, and revenues. When companies miss these benchmarks, subsequent investors may insist on lower company valuations due to concerns over inexperienced management, early hype versus reality, and questions about a company’s ability to execute its business plan.

What is conversion?

When companies raise funds through a preferred stock financing, early-stage investors often receive certain “price protections” to ensure those investors will enjoy a fair share of equity ownership even if the company later raises funds at a lower valuation. These protections affect how preferred stock can convert into common stock. If your company’s preferred stock financing round utilized the form preferred stock financing documents provided by the National Venture Capital Association (NVCA), Section 4 of your company’s current Certificate of Incorporation (or equivalent document) outlines the process by which preferred stock would convert into common stock.

Often, during a company’s liquidation after an exit event, a preferred stockholder will either (a) receive a liquidation preference equal to its initial investment amount (or some multiple thereof) or (b) convert its shares of preferred stock into common stock and give up its liquidation preference. (This is referred to as a non-participating preferred structure. Alternatively, in a participating preferred structure, the preferred stock might receive both the return of its initial investment (or some multiple thereof) and participate in the distribution of remaining assets with the common stockholders.)

Adjustments to the Conversion Price During a Down Round

As a default, preferred stock will convert into common stock based on the ratio of the “original issue price” of the preferred stock (the amount investors originally paid for the stock) by the “conversion price.” The conversion price is a term used to balance the potential dilution caused by certain corporate activity. At the initial closing of a financing round, the original issue price and the conversion price are the same, so, as a default, preferred stock converts into common stock at a one-to-one ratio. A Certificate of Incorporation implemented as part of a preferred stock financing round will generally require that, upon the occurrence of certain dilution events, a corporation must adjust the conversion price of a particular class of preferred stock. Several of these triggering events involve the corporation’s issuance of additional shares of stock. A down round will usually trigger an adjustment to the conversion price of each class of existing preferred stock with a current conversion price greater than the price per share of the newly-issued preferred stock.

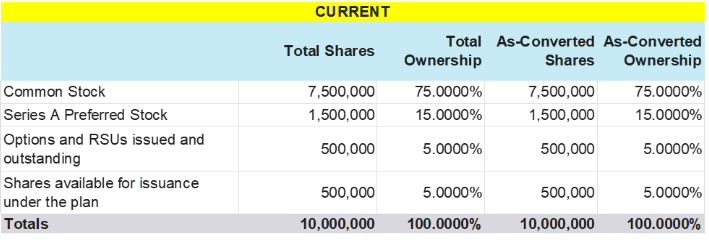

To understand the effects of such an adjustment on a corporation’s capital structure, consider the following example: Company A previously sold 1,500,000 shares of Series A preferred stock to investors at a price per share of $20, and such shares represent 15% of the current, fully-diluted capitalization. To date, no diluting event has occurred that would trigger any anti-dilution adjustment to the conversion of Series A preferred stock. So, if converted into common stock, the Series A preferred stock would convert at a one-to-one ratio.

Company A now intends to raise $10,000,000 through the sale of a new class of Series B preferred stock at a pre-money valuation of $90,000,000. As outlined below, given Company A current has 10,000,000 outstanding shares of fully-diluted common stock, the Series B round, as proposed, will involve the sale of 1,111,111 shares of Series B preferred stock at a price per share of $9.00, less than half the per share price of the Series A preferred stock.

Assuming Company A’s Series A preferred stock financing round utilized the standard NVCA form Certificate of Incorporation, this down round would trigger an adjustment to the conversion calculations for the Series A preferred stock. Fortunately, the NVCA Certificate of Incorporation clearly outlines how Company A will calculate the adjusted Series A conversion price. (The specific calculation is too detailed to describe in this blog post, but it is usually described in Section 4.4 of the NVCA Certificate of Incorporation.) The Series A conversion price would be proportionally reduced to reflect the extent to which the Series A preferred stock is diluted by the surplus Series B preferred stock issued by nature of the down round. In this example, the Series A conversion price would decrease from the original per share issue price of $20 to approximately $18.85.

Moving forward, if the Series A preferred stock were to convert into common stock, instead of converting at a one-to-one ratio, for every 18.85 shares of Series A preferred stock, a preferred stockholder would receive 20 shares of common stock. As shown below, this significantly increases the Series A stockholders’ as-converted ownership. The 1,500,000 shares of Series A preferred stock would convert into 1,591,664 shares of common stock, representing an increase from 13.5% ownership generally to 14.2% ownership on an as-converted basis. For a company with a valuation of $100,000,000, that adjustment could represent an additional $700,000 payout to the Series A stockholders upon a sale of the Company (depending on how distributions are made in the Certificate of Incorporation).

Best practices for approaching a down round

If your company is considering a down round, the following are some best practices to consider:

Communicate early-on with existing shareholders and the incoming investor about the effects of a down round on the corporation’s capitalization table. Make sure your attorney properly reflects the conversion metrics in the pro forma capitalization table for your fundraising round.

Ensure the corporation has sufficient shares of authorized common stock available in case the preferred stock converts into common stock.

Comply with all notice provisions required by state law and in the corporation’s existing Certificate of Incorporation. Delaware law, for example, requires corporations to notify all stockholders of any written or other informal action taken by a majority of the stockholders. Additionally, the Certificate of Incorporation often requires that companies issue a certificate to all holders of preferred stock promptly informing them of an adjustment to the conversion price of any preferred stock class.

Account for the adjusted conversion price in your electronic capitalization table or other governance ledgers.

As always, it is critical that your corporation formally engage legal counsel experienced in venture capital financing to advise you about the various risks, benefits, and other considerations associated with a financing round. The Fourscore team is available and happy to assist your company through this pivotal stage of growth.

Headquartered in the Research Triangle region of North Carolina, Fourscore Business Law serves entrepreneurs and businesses in the Triangle, throughout the Southeast and in Silicon Valley / San Francisco. We also represent venture capital funds and other investors who invest in companies throughout the U.S. The idea of delivering maximum impact in a simple and succinct manner is what we’re calling the Fourscore Principle. And that is what Fourscore Business Law is based on. Our clients operate in a broad range of industries including tech, IoT, consumer products, B2B services and more. Questions? Shoot us an email or give us a call at (919) 307-5356. Your first call is on us.